Many people worry that pursuing their legal rights will hurt their credit or ability to buy another car. Here’s what you need to know: filing a California Lemon Law claim does not appear on your credit report. You can hold the manufacturer accountable without sacrificing your financing options.

Understanding what shows on credit reports, how lenders view manufacturer buybacks, and simple preparation steps makes your next purchase stress-free. The Barry Law Firm helps California families recover every dollar while protecting their financial future.

Will a California Lemon Law Claim Show Up on Your Credit Report?

The short answer is no. Does filing a Lemon Law claim in California show up on your credit report? Filing a California Lemon Law claim will not appear on your Equifax, Experian, or TransUnion credit file. Your credit history tracks your debts and payment behavior, not consumer claims you file against car manufacturers.

What Your Credit File Actually Tracks

The Consumer Financial Protection Bureau explains that credit reports include payment history, current debts, credit inquiries, and public records like bankruptcies. These reports focus on your financial obligations and how you handle them. When you pursue compensation for a damaged lemon, you are using your legal rights, not creating a debt that credit agencies would track.

Why Lemon Law Claims Stay Off Your Credit History

Unlike unpaid debts or missed payments, filing a Lemon Law claim creates no financial obligation that credit agencies would monitor. Civil judgments are no longer included on standard credit reports. They also do not directly affect credit scores. A Lemon Law claim is simply a civil action seeking recovery from the manufacturer who sold you a defective vehicle.

Protecting Your Credit During the Process

The real threat to your credit score is falling behind on loan payments because your car keeps breaking down. If you stay current on your auto loan while pursuing your case, your credit should remain unaffected. This means you can pursue the safe, reliable vehicle your family deserves without worrying about credit damage. Get free legal help to protect both your rights and your financial future.

How Lemon Law Buybacks Affect Financing Your Next Car

Many people worry that a manufacturer buyback will make it harder to get approved for their next car loan. The good news is that lenders care much more about your ability to pay than your vehicle history. When you apply for financing, lenders focus on the basics of whether you can make payments on time.

- Lenders prioritize your credit score and income – Your credit score, monthly income, and debt-to-income ratio matter far more than whether you received a manufacturer buyback for a defective vehicle

- A buyback often improves your credit profile – When the manufacturer pays off your existing loan as part of the buyback calculation, it removes a problematic account from your credit report, especially if you stayed current on payments

- Documentation prevents underwriter confusion – Keep a brief explanation letter about the manufacturer buyback, your payment history, and any compensation received to quickly address any lender questions

- Title branding affects the old car, not you – While California requires title branding for buyback vehicles, this appears on the vehicle’s history, not your personal credit file

- Buybacks differ from repossessions – Unlike a repossession that damages credit for years, a manufacturer buyback resolves your loan through legal remedy, not missed payments

Will a Lemon Law buyback make it harder to get approved for a car loan in California? Rarely. Lenders understand that defective vehicles happen, and a properly documented buyback often strengthens rather than weakens your financing application.

What Dealers and Lenders Actually See—and How to Prepare

When you’re ready to buy your next vehicle, dealers and lenders focus on your creditworthiness, not your legal claim history. They cannot see that you filed a Lemon Law claim on your credit report. What they may see is a branded title on your old vehicle’s history, which stays with that car, not with you as a borrower.

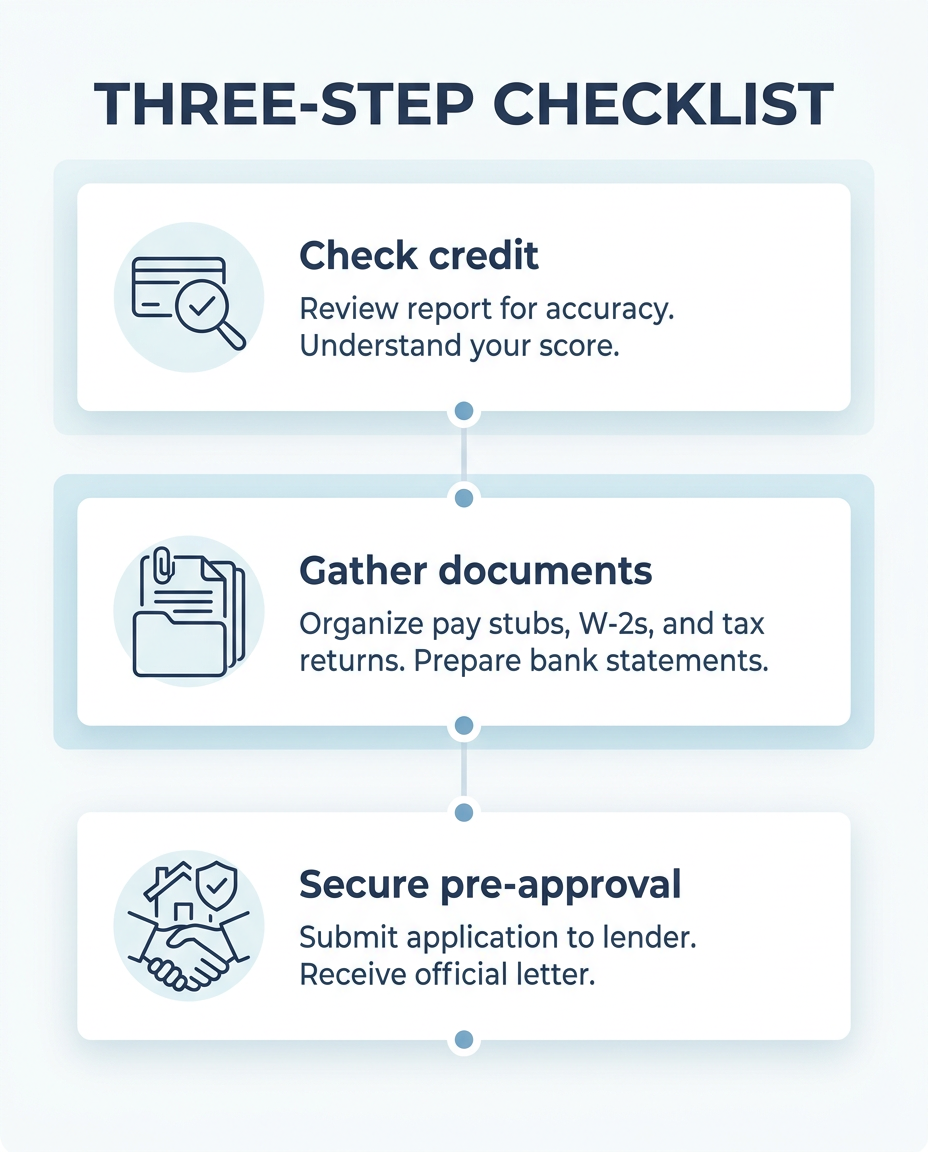

Follow this simple preparation plan to make financing your next car smooth and stress-free:

- Check your credit report first – Verify that your auto loan payments appear current and that no errors exist from your defective vehicle situation

- Gather your buyback documentation – Create a one-page summary showing the manufacturer paid off your loan and any refund amount using our buyback calculator as a guide

- Collect 17 months of payment history – Show lenders you stayed current on payments despite vehicle problems (most lenders review 12-24 months to assess payment patterns)

- Get pre-approved before shopping – Secure financing terms in advance so you can focus on finding a safe, reliable vehicle for your family

- Prepare a brief explanation – Keep it simple: “The manufacturer bought back my defective vehicle and paid off the loan per California Lemon Law”

Most lenders care about your ability to make payments, not whether you exercised your legal rights. A successful Lemon Law buyback often improves your financial position by removing a problematic loan and putting money back in your pocket.

FAQs: Credit, Buybacks, And Your Next Vehicle

People facing vehicle defects often worry about protecting their credit while securing safe, reliable transportation. These California lemon law credit and buyback FAQ answers address the most common concerns about how pursuing your legal rights affects credit scores and future financing decisions.

Does a Lemon Law claim lower my credit score?

No, filing a California Lemon Law claim does not appear on your credit report or affect your credit score. Credit bureaus track debts and payment history, not consumer protection claims against manufacturers. You have the right to hold manufacturers accountable without credit consequences.

Will a branded title or manufacturer buyback on my old car follow me to my new loan?

A branded title affects the vehicle’s resale value but has no impact on your personal creditworthiness. Lenders evaluate your credit score and income, not previous vehicle issues. Lemon Law buybacks often improve your financial position by eliminating problematic monthly payments.

Should I wait until my Lemon Law case is resolved before shopping for a replacement vehicle?

You can shop anytime, but resolution helps with financing. A successful buyback provides funds for a down payment and eliminates your current loan obligation. Many families secure pre-approval while their case progresses, and our bilingual team can guide you through timing decisions.

If I missed payments because the car was undrivable, what can I do before applying for a new loan?

Keep records showing how vehicle problems caused missed payments. Contact your lender to explain the situation and request payment forgiveness or account corrections. Lemon Law attorneys can help recover damages for transportation costs, and manufacturers pay all legal fees.

Can dealers see my previous Lemon Law claim when I shop for a new car?

Dealers cannot access your claim history through credit reports or standard background checks. They may see branded titles on specific vehicles, but your consumer protection actions remain private. Come prepared with documentation showing responsible payment history on your current loan.

Move Forward With Confidence—Free, Risk-Free Legal Help

Filing a California Lemon Law claim protects your rights without damaging your credit or ability to finance your replacement vehicle. The claim itself never appears on credit reports, and manufacturers cover all legal fees in your case. With proper documentation and preparation, your new car purchase can proceed smoothly.

What matters most is getting your family back into a safe, reliable vehicle without financial worry. Learn more about how Lemon Law claims affect your ability to buy or lease another car, then contact The Barry Law Firm for your free consultation and case review to secure the California Lemon Law legal help to buy another car with confidence.